The end of dollar hegemony?

This is the CIA headquarters at Langley, Virginia. Twenty minutes east, across the Potomac, is the White House. And seventy minutes southwest lies the SWIFT data centre at Culpeper, which logs its global cross-border transactions.[1] The proximity of these sites is no coincidence. Since 1944, American financial power has been a key geopolitical weapon.  Figure 1: CIA HQ (AKA George Bush Center for Intelligence).

Figure 1: CIA HQ (AKA George Bush Center for Intelligence).

Here, the main component is the US dollar. Vital commodities, including hydrocarbons and precious metals, are priced in dollars. And by controlling global money flows and overseeing one quadrillion dollars of annual international transactions, Washington can freeze out its enemies via unilateral sanctions.[2] Figure 2: SWIFT data facility, Culpeper, Virginia.

Figure 2: SWIFT data facility, Culpeper, Virginia.

And that is precisely the problem. Nowadays, many states see dollar hegemony as a relic of American primacy and seek to develop alternative financial infrastructures. Most are centred around China, the only economy large enough to counterbalance the United States. Dedollarisation is fast expanding via bilateral, multilateral, and institutional arrangements. So, what is the nature of the dollar matrix? How did Washington gain and wield dollar power? And how deep does the rabbit hole go?

Render unto Caesar[3]

Money is the power to command others.[4] A social institution and public good, historically, it was tied to precious metals. But since coinage was liable to clipping, wearing, and debasement, its social power derived not from its metal content but from the state whose mark it bore.[5] Figure 3: British Empire (interwar).

Figure 3: British Empire (interwar).

In an anarchic global system, though, there can be no world state.[6] And since monetary systems are inherently national, global money regimes reflect the interests of the currency-issuing great powers.[7] Figure 4: French Empire (interwar).

Figure 4: French Empire (interwar).

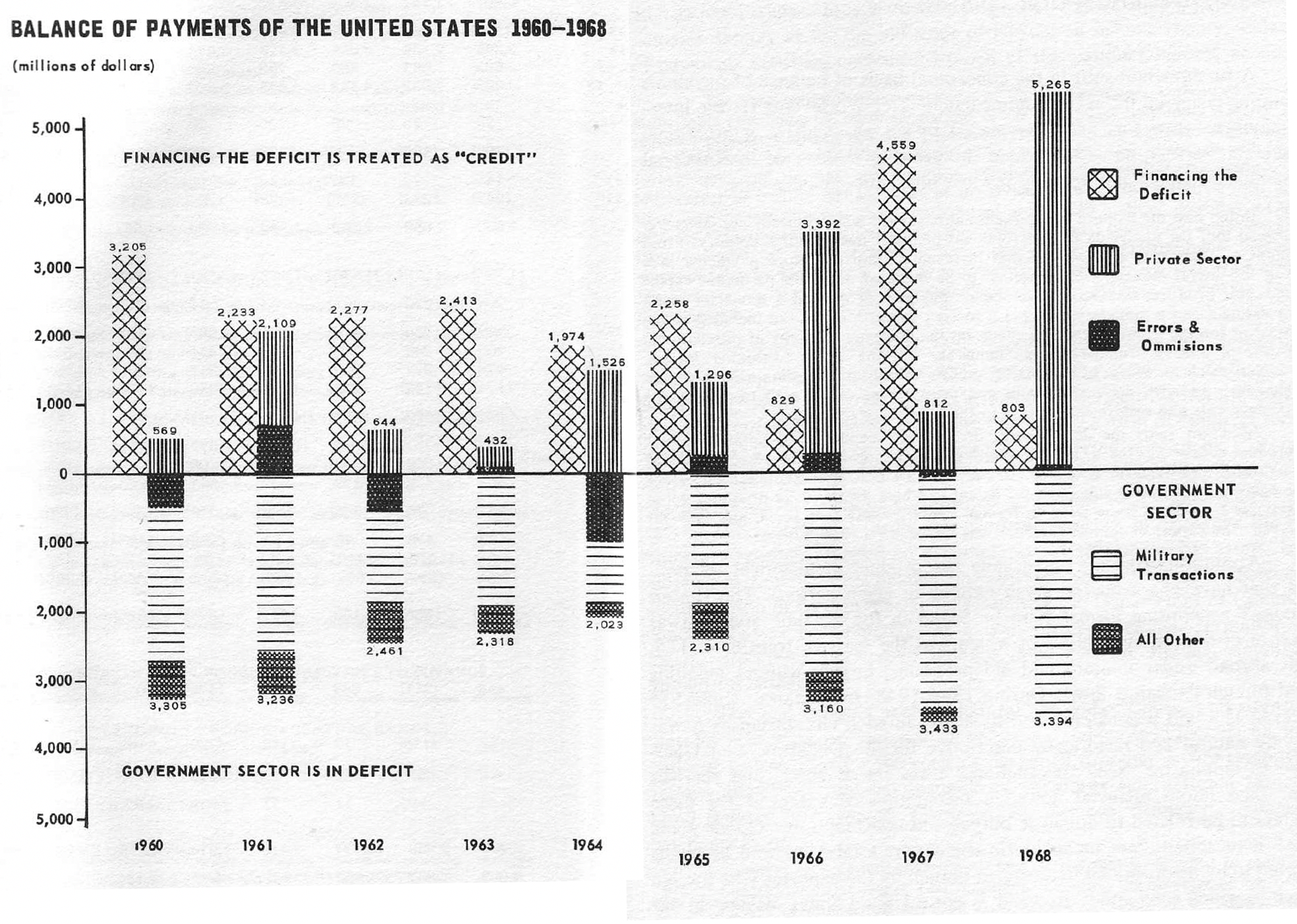

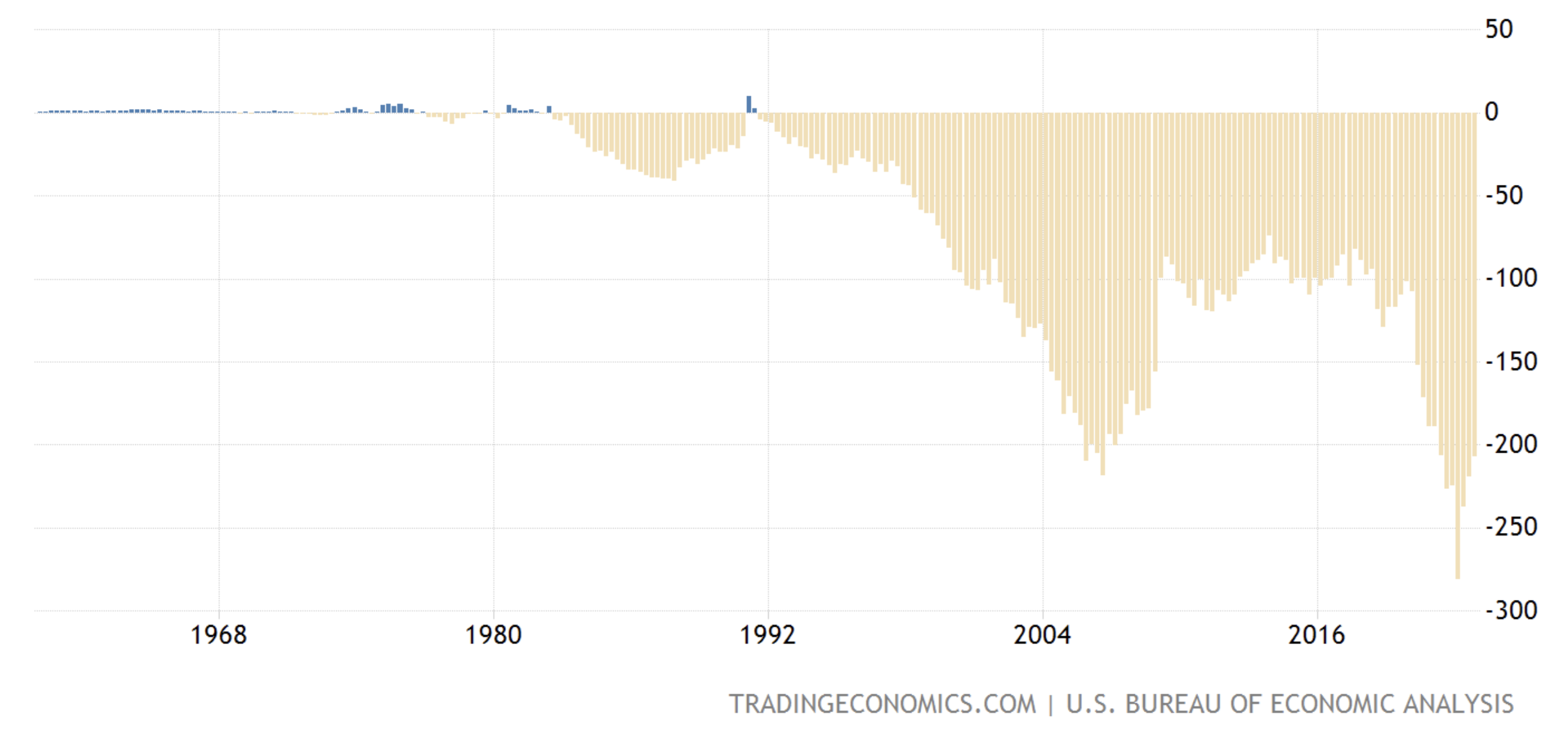

Since 1944, monetary power has centred in the United States. With Western Europe in tatters and the East falling behind the iron curtain,[8] Washington used creditor power to pry open Britain and France’s imperial trading blocs.[9] Postwar reconstruction loans were predicated on importing American food and manufactures and granting Washington veto power at lending institutions, including the IMF and World Bank.[10] Figure 5: United States balance of payments (1960-68), Source: Michael Hudson.

Figure 5: United States balance of payments (1960-68), Source: Michael Hudson.

A system of fixed exchange rates, convertible with gold at USD 35/oz, held the system in place. But while Washington initially enjoyed a major trade surplus,[11] NATO expenditure and military buildups in Korea and Vietnam dragged its international payments into the red. By 1964, America’s payments deficit was due solely to overseas military spending. But the formation of vested interests,[12] and the insistence that such outlays were vital to ‘national security’, prevented Washington from pulling the plug.[13]

As American allies exchanged their dollars for gold, convertibility came unstuck, as the volume of circulating dollars soon exceeded the legal limit of four times Washington’s gold stock. And after exhausting every expedient available to keep convertibility afloat, in August 1971, the Nixon Administration abandoned gold and devalued the dollar by ten per cent.[14]

In so doing, Washington stumbled upon a geopolitical masterstroke.[15] Foreign central banks could no longer check the US by exchanging dollars for gold. But nor could they repudiate the dollar as a means of payment. Doing so would render their vast dollar holdings worthless. And since American corporate stocks were too risky,[16] and its real estate too illiquid, foreign central bankers’ only sensible option was to recycle their dollars into interest-bearing US Treasury securities.[17]

Failure to do so would have also caused a dollar oversupply, granting American firms a competitive devaluation against European industry. Washington’s allies thus had no choice but to accept dollar hegemony, leading Nixon’s Treasury Secretary, John Connally to quip that America’s dollar had become the world’s problem.[18]

Critical mass

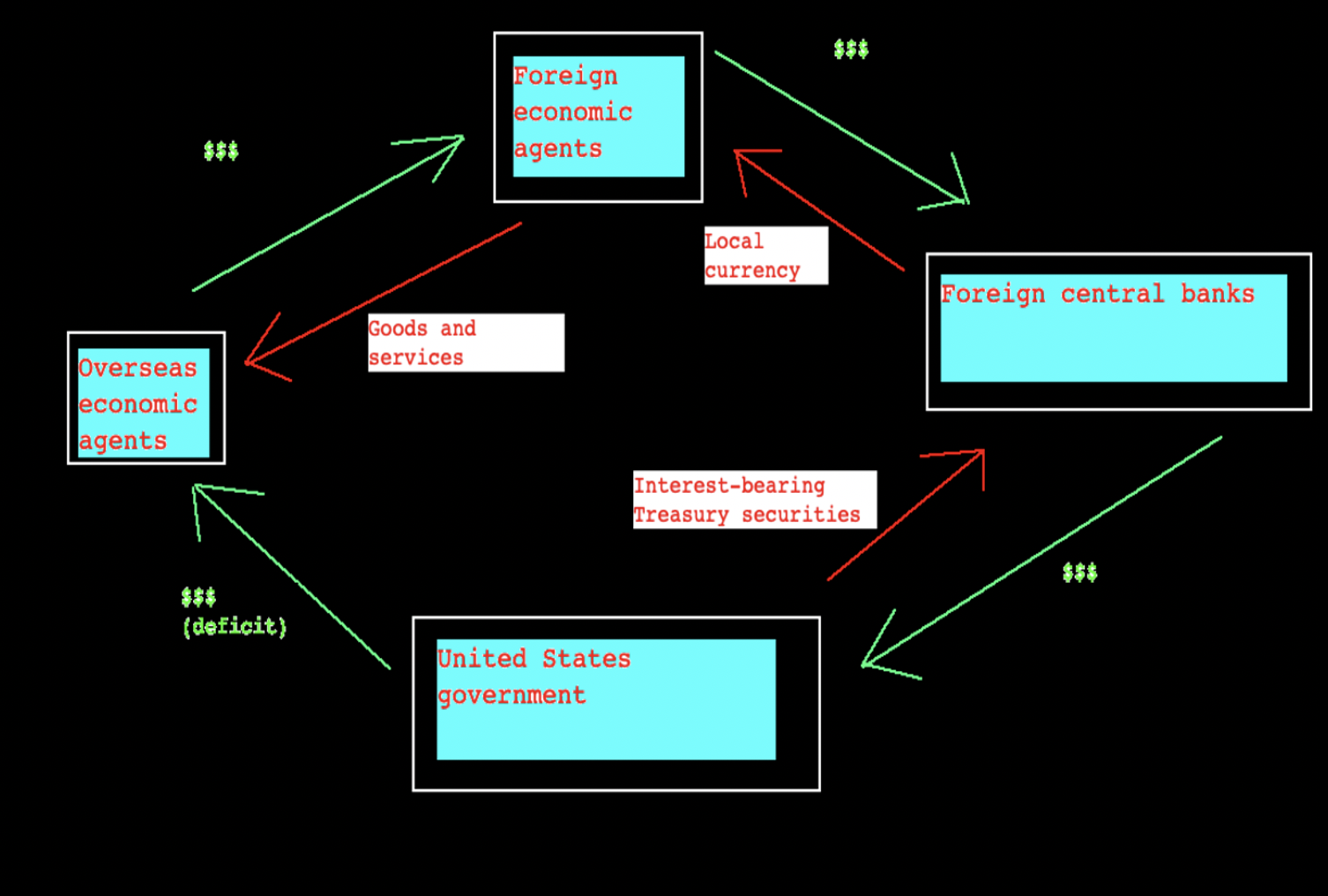

Untethered from gold, Washington pursued overseas military spending without constraint. Dollars spent overseas would be exchanged for local currency, flowing into foreign central banks, and cycling back to the US as Treasury security purchases. There was no theoretical limit to this new circular flow. Figure 6: Treasury security standard, circular flow.

Figure 6: Treasury security standard, circular flow.

Effectively, the perpetual rollover of American debt acted as a military subsidy. American strategists could encircle Russia and China[19] with 800 military bases,[20] knowing the money spent would simply boomerang home. All while fear of an international monetary breakdown prevented other states from calling America’s bluff. The United States’ debtor status thus cemented American power. And its dollar-making capacity excluded it from the austerity rules it applied to other dollar-debtor states via the IMF and World Bank.[21] Figure 7: American military bases in Eurasia (Source: World Beyond War).

Figure 7: American military bases in Eurasia (Source: World Beyond War).

A 1974 deal with Saudi Arabia bolstered this power further. Riyadh would sell oil in dollars and recycle the proceeds into Treasuries.[22] Combined with American agricultural dominance, this meant unilateral dollar sanctions could strangle Washington’s enemies from food and energy imports. Figure 8: United States current account balance.

Figure 8: United States current account balance.

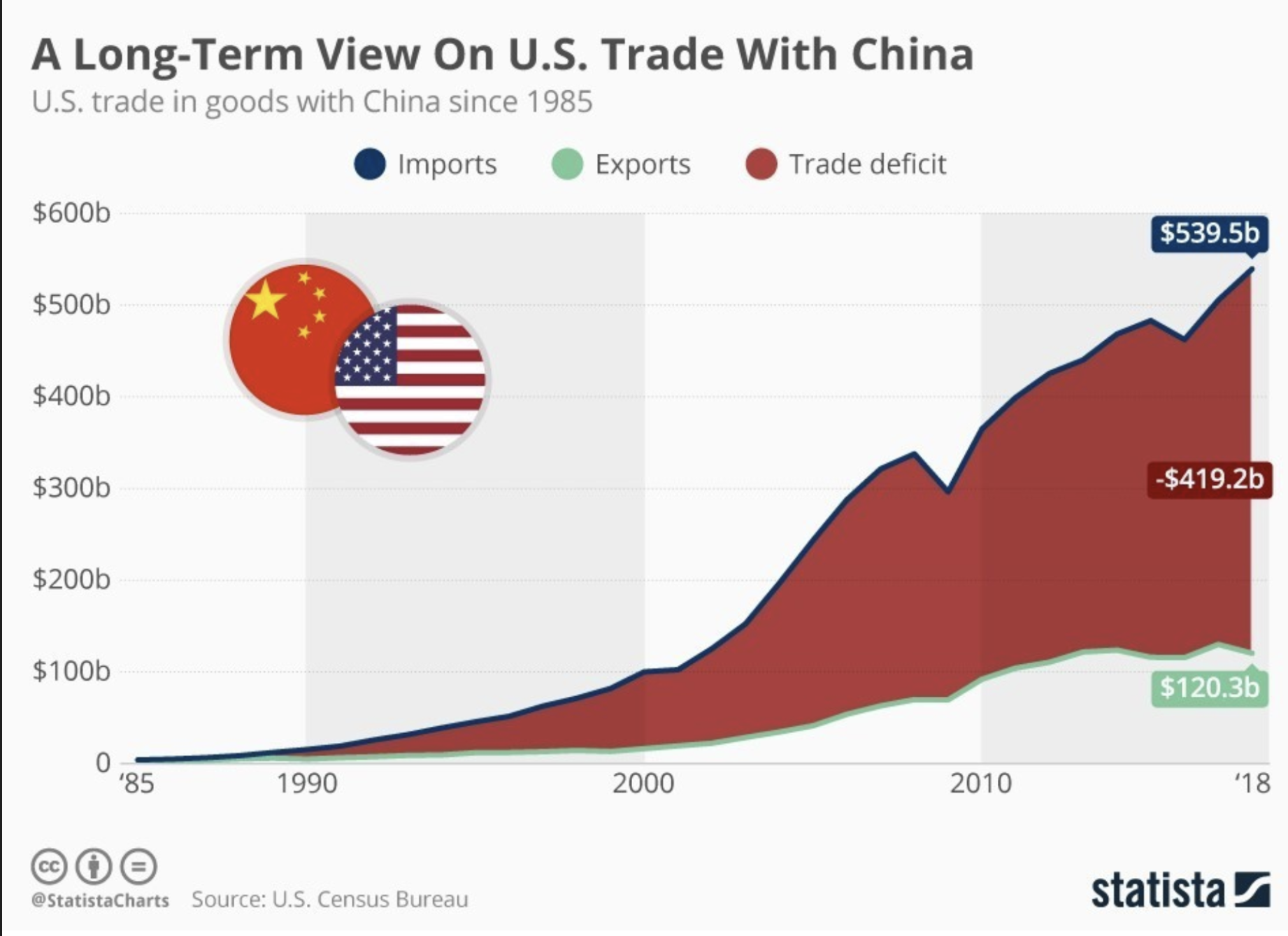

Naturally, Third World[23] states saw this system as inequitable, instead pushing for a New International Economic Order, though they initially lacked the hard power to implement it.[24] Ironically, though, it was American corporations’ offshoring their production to China, in search of lower wages, that eventually made this project possible. Figure 9: Growth in American imports of Chinese goods.

Figure 9: Growth in American imports of Chinese goods.

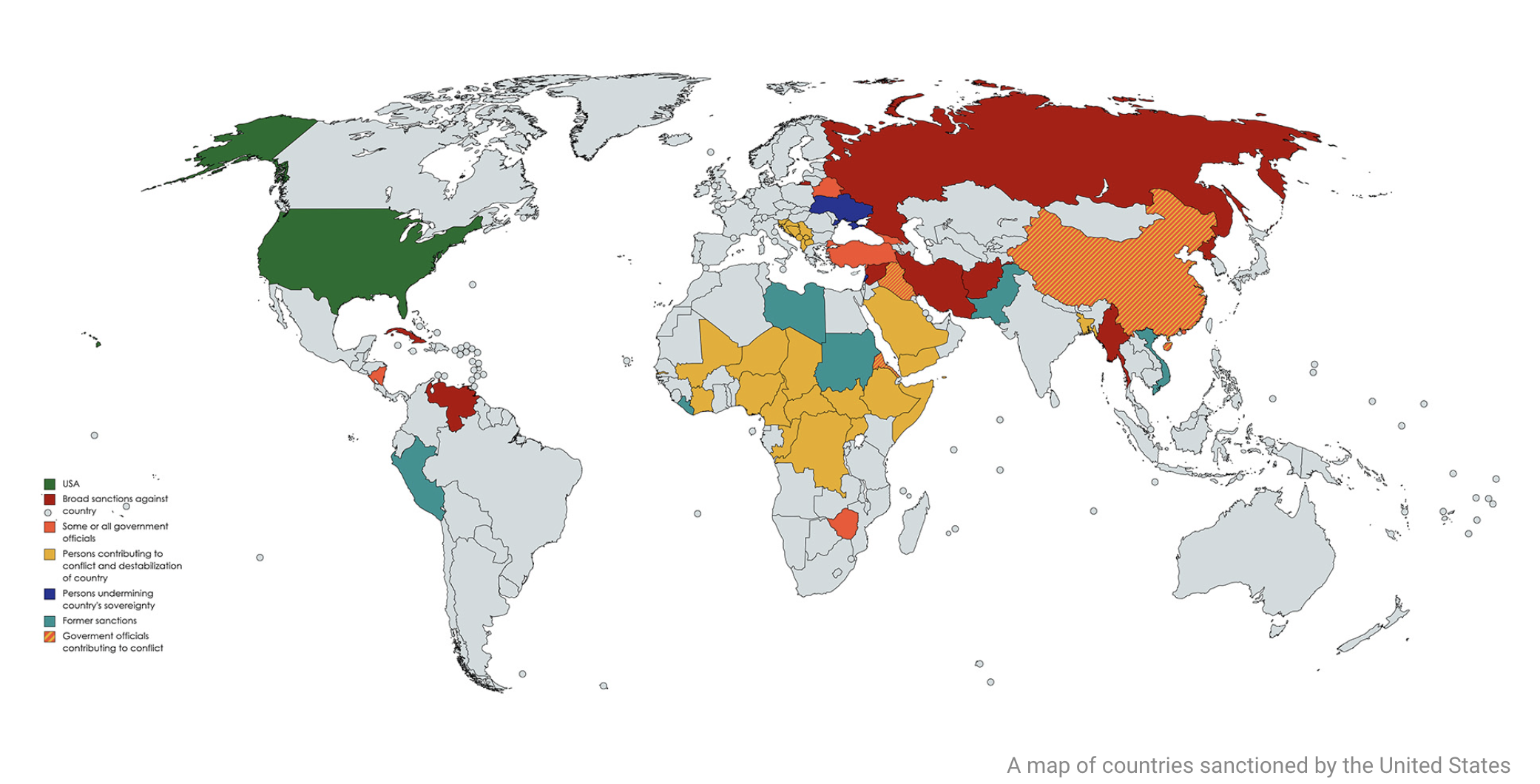

Mistaking money for national wealth, Washington saw profit rates increase. But the real wealth of nations is their productive capacity.[25] And as North America deindustrialised, Washington’s growing import-dependency and China’s industrial development became a geopolitical friction point.[26] Figure 10: US-sanctioned countries.

Figure 10: US-sanctioned countries.

Beijing also grew wary of funding its own encirclement via the Treasury security standard. But its exposure to the dollar system kept it in an uneasy balance, not least due to its holding of USD 1 trillion of American debt.[27] Instead, it was China’s partners who provided the catalyst for dedollarisation.

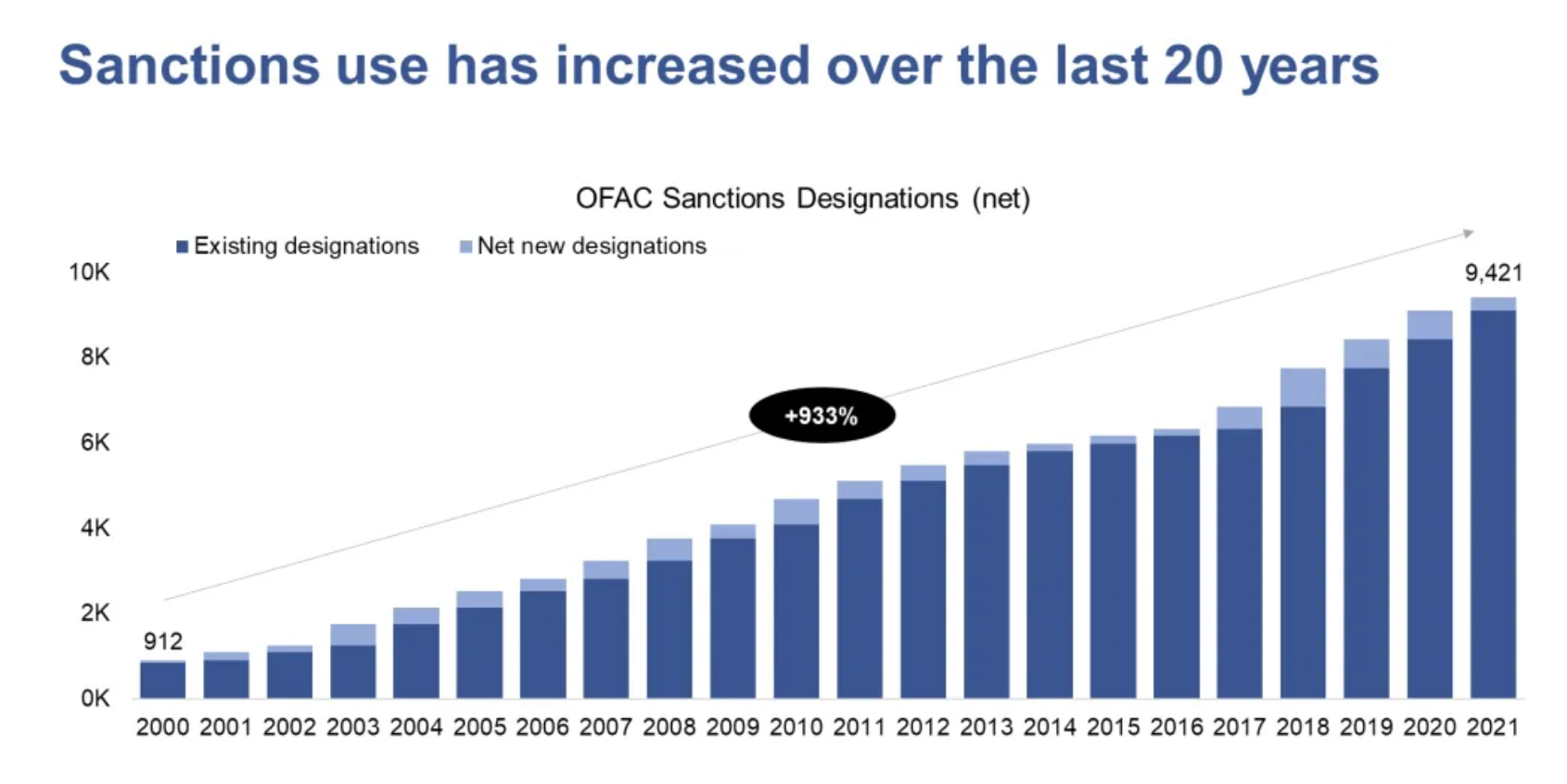

Since 2000, American sanctions designations have risen by 900 per cent,[28] escalating following Russia’s annexation of Crimea,[29] and expanding to Chinese technology firms like Huawei. Initially, most major economies swallowed these measures. But the freezing of Iranian, Venezuelan, and Afghan sovereign assets pushed the envelope.[30] And, in 2022, the tipping point came when Washington seized USD 300 billion in Russian assets,[31] and suggested a post-hoc revision of US law to disperse the funds for Ukraine’s reconstruction.[32] Figure 11: Number of US sanctions designations, OFAC (Source: Timothy Taylor).

Figure 11: Number of US sanctions designations, OFAC (Source: Timothy Taylor).

This decision, more than any other, ended dollar hegemony. Though Washington may dislike Russia’s invasion of Ukraine, the hard fact is countries will not bank with a state that seizes sovereign assets.[33] A modicum of trust, even between enemies, is needed. This trust is now gone. And since many predict a Sino-American conflict soon, Beijing’s belated dedollarision efforts are designed to avoid Russia-style sanctions. Thus, for now, bilateral and multilateral dealmaking allows China to manage its dollar decoupling, while providing states like Russia and Iran with an economic lifeline.

My enemy’s enemy

This has given smaller states the green light to follow suit, a fact acknowledged even by the US Treasury.[34] Central bank dollar reserves are proportionally declining, while Russia, China, and the EU are building SWIFT alternatives like SPFS, INSTEX and CIPS. Figure 12: Proportion of dollars in central bank reserves.

Figure 12: Proportion of dollars in central bank reserves.

Beijing has struck a CNY 130 billion (worth USD 19 billion)[35] currency swap deal with Argentina,[36] freeing up the latter’s dollars to service its IMF debts. And its status as a broker in Iran-Saudi Arabia talks has given it the diplomatic heft to match its buying power as the world’s top oil and petrochemical importer. Riyadh is considering selling oil in renminbi. And Qatar has already settled gas purchases in yuan.[37]

Over time, such arrangements could spread through groupings like the Shanghai Cooperation Organisation, which accounts for one-fifth of global GDP.[38] But the most significant grouping is BRICS, containing two-fifths of the world’s population, one-quarter of its GDP, and 16 per cent of its commerce, and which is openly committed to dedollarisation.[39]

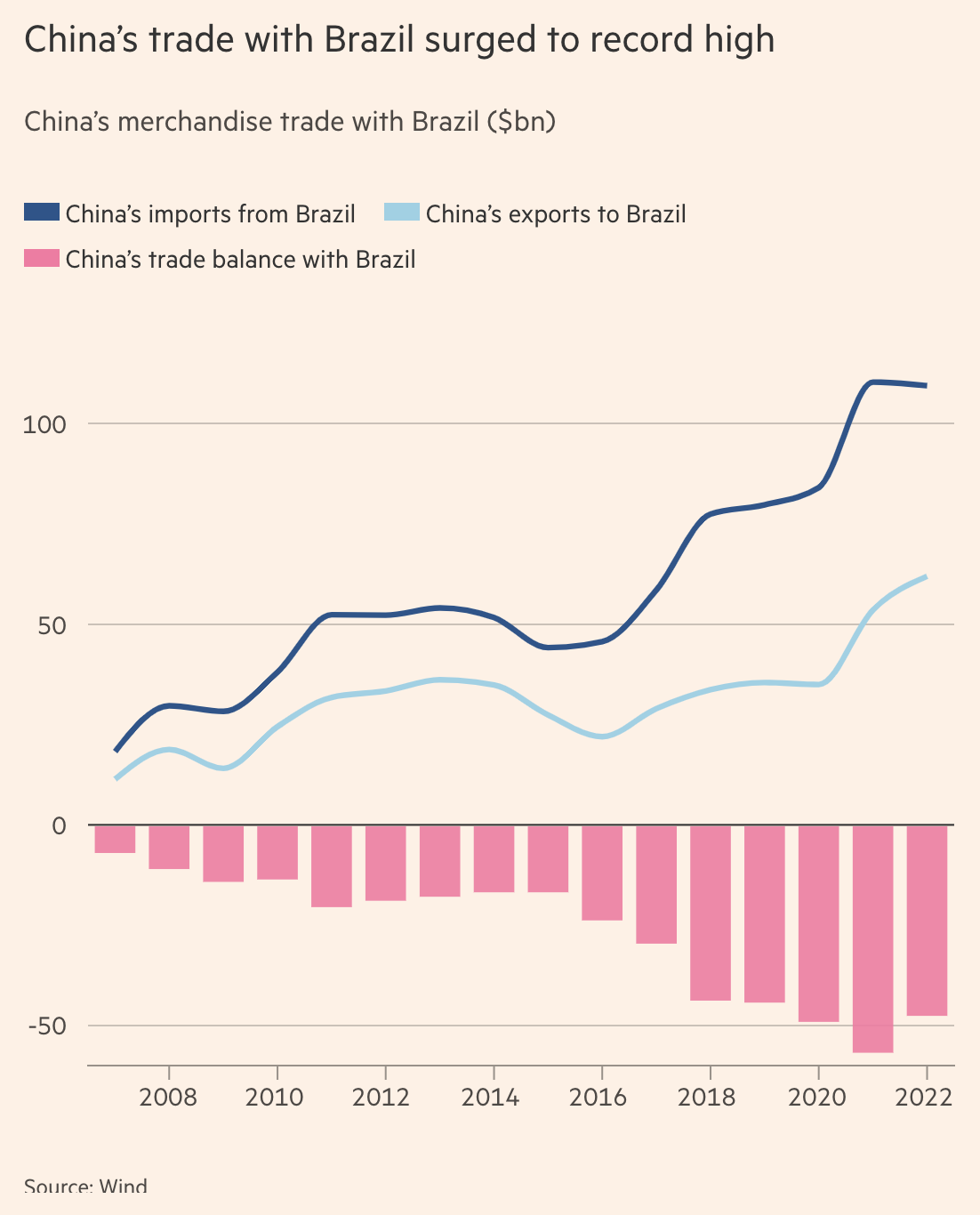

The China-Brazil nexus is especially important. Brazil’s commodity-producer status meant it conducted over USD 150 billion of trade with China in 2022. And in March 2023, the two countries agreed to trade in local currencies,[40] a move accompanied by the appointment of Brazilian economist and former president Dilma Rousseff as head of the New Development Bank. Rousseff aims to provide one-third of NDB loans in local currencies, facilitating easier debt repayment.[41] And 19 states are looking to join BRICS, including Argentina, Egypt, and Indonesia.[42] Figure 13: China’s trade with Brazil and growing trade deficit off the back of Brazilian commodity exports.

Figure 13: China’s trade with Brazil and growing trade deficit off the back of Brazilian commodity exports.

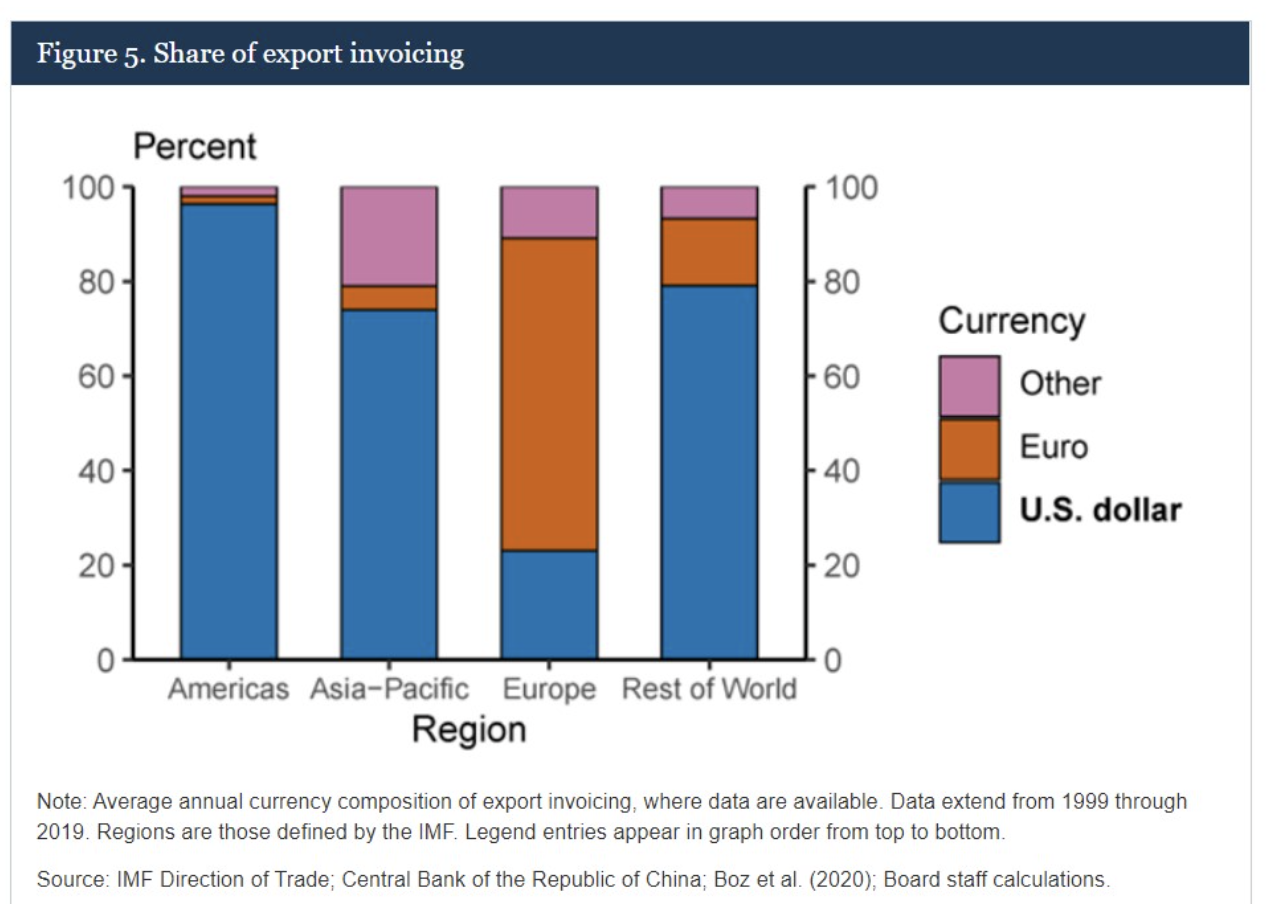

Meanwhile, Argentina and Brazil are moving towards a common trade currency, called the sur. Unlike the euro, the sur will not replace domestic currencies. But like the euro, it could potentially withdraw Latin America from the dollar zone. The dollar accounted for more than 96 per cent of regional cross-border payments between 1999 and 2019. But if the sur catches on, this could fall to similar levels to Europe, where it only accounts for one-fifth.[43] Figure 14: Regional usage of dollar for trade (1999 – 2019).

Figure 14: Regional usage of dollar for trade (1999 – 2019).

Other developments, like central bank digital currencies, could create parallel payments networks independent of dollar influence.[44] But in the interim, gold will likely form an expedient.[45] Beijing has recently begun moving away from Treasury purchases and towards building its gold stock, accumulating 1880 tonnes by April 2023.[46]

The emphasis on gold hints at something more general. China regulates credit as a public utility, deploying it selectively for developmental, political, and strategic objectives. Flooding the world with yuan would make Chinese policy hostage to competing priorities, something Beijing will not countenance. So, while the prevalence of yuan will chip away at the dollar, it will not replace it as the world’s money.[47]

Currency orders reflect the balance of power. Multipolarity is already here. And multipolar currency regimes are not far off. The US dollar is not going anywhere but its exorbitant privilege[48] is winding down. This will blunt its use as an economic weapon[49] and shift America’s military spending burden onto its tax base, thereby exposing it to domestic political pressures. The twentieth century was the American century. But the twenty-first will not be the American, Russian, or Chinese century – only the multipolar one. Yet, this represents nothing more than a resumption of historical normalcy, returning the world from the strange detour it took in the wake of the Great War.

This article formed the basis of this video by CaspianReport.

[1] There are three SWIFT data centres, one in Culpeper Country, Virginia, one in Zoeterwoude, Netherlands, and one in Thurgau, Switzerland. Security at the Culpeper facility has been described as ‘James Bond-level’ and ‘like Fort Knox’. See Katy Burne and Robin Sindel, ‘Hackers run through holes in Swift network’, Wall Street Journal (30 April 2017) https://archive.is/20170505101049/https://www.wsj.com/articles/hackers-ran-through-holes-in-swifts-network-1493575442#selection-4389.6-4389.20.

[2] Fernandes, Clinton, ‘Australian foreign policy after COVID-19’ (Youtube lecture, 1 June 2020) https://www.youtube.com/watch?v=3fek56p46A8.

The ‘quadrilion dollars’ figure relates to transactions passing through CHIPS and Fedwire in 2018.

Moreover, sanctions are ‘unilateral’ because American allies follow them for fear of secondary sanctions. For instance, all of Washington’s allies, except Israel, condemn its sanctions policy on Cuba at an annual UN General Assembly vote. But they nonetheless comply with them for fear of secondary sanctions.

[3] Jesus, as quoted in Matthew 22:22. The quote is ‘Render therefore unto Caesar the things which are Caesar’s; and unto God the things that are God’s.’ This passage of the New Testament is basically pro-Roman propaganda telling people to pay the king’s taxes in the coin that bears his mark.

[4] Smith, Adam, The Wealth of Nations (1776) bk I, ch. V. “The power which [wealth] immediately and directly conveys to [a person], is the power of purchasing a certain command over all the labour, or over all the produce of labour which is then in the market.”

[5] Desai, Radhika and Michael Hudson, ‘Beyond dollar creditocracy: A geopolitical economy’ (September 2021) 97 Real-World Economics Review 20, 22.

See also Karl Marx, Capital (vol. 1, 1867) 222-6.

To be sure, gold coinage does carry an intrinsic value that pure fiat money does not by virtue of its precious metal content. But this is insufficient to explain why such coinage can have a higher face value than its actual precious metal content, or why currency with no precious metal content can function as money at all. The reason is that the law privileges it as legal tender. The historical use of precious metals was actually more of an anti-forgery measure since precious metals cannot be counterfeited.

[6] Mearsheimer, John, The Tragedy of Great Power Politics (W.W. Norton & Co, 2nd ed., 2012) 30. International anarchy is a ‘bedrock assumption’ of realism.

[7] Desai and Hudson, 24.

This was also the theme of the CFA franc paper. The CFA franc’s overvaluation, and the use of the French Treasury as a chokepoint between the franc zone and the global economy, was designed to provide France with raw materials at sub-market prices and soak up its output of higher value-added products. The net effect of this is a wealth transfer to the metropole.

[8] Soviet Russia established its own creditocracy by controlling the rule-making bodies of trade, investment, and finance to garner economic predominance over other Comecon states. But this system functioned rather differently, and was walled off from the American-led dollar system.

[9] Washington did this by insisting on ‘free trade’. In the context of the destruction of Europe’s industrial and agricultural base during wartime, and the breakneck development of American industry off the back of the total war effort, ‘free trade’ meant retaining American economic hegemony in Europe.

Of course, states tend to get second thoughts about free trade when it is geopolitically disadvantageous. By the 1950s, the US was already flouting free trade via agricultural market interventions. And this is one of the reasons why Europe implemented its Common Agricultural Policy in 1962. More recently, the United States’ inability to compete on free trade terms led Donald Trump to withdraw the US from the TPP. And Joe Biden has followed suit by enacting protective measures pertaining to American high-technology industries.

[10] Desai and Hudson (2021) 29. This was a theme of American participation in postwar institutions. The US Congress insists that Washington, at bare minimum, have veto power in any substantial organisation it joins. This is why it did not approve American membership of the League of Nations. And it is also why following World War 2, the US advocated for veto power at the UN Security Council, IMF, World Bank, and other institutions.

[11] Hudson, Michael, Super-Imperialism: The Economic Strategy of American Empire (Islet, 3rd edition, 2021) 12-13.

[12] That is, the ‘military-industrial complex’, in the words of President Dwight D. Eisenhower, who noted its growing influence in his farewell address: ‘In the councils of government, we must guard against the acquisition of unwarranted influence, whether sought or unsought, by the military-industrial complex. The potential for the disastrous rise of misplaced power exists and will persist.’

See Eisenhower, Dwight (United States President) ‘Farewell address’ (speech, 17 January 1961) https://www.archives.gov/milestone-documents/president-dwight-d-eisenhowers-farewell-address.

[13] Hudson, 13-17.

[14] Though, at the time, Nixon stated that this was only a temporary decision: ‘I have directed Secretary [John] Connally to suspend temporarily the convertibility of the dollar into gold or other reserve assets, except in amounts and conditions determined to be in the interest of monetary stability and in the best interests of the United States.’

See Nixon, Richard (United States President) ‘The challenge of peace’ (speech, 15 August 1971) https://youtu.be/ye4uRvkAPhA.

[15] Hudson, vi.

[16] Washington probably would not have allowed them to, anyway, for strategic reasons.

[17] Ibid., 18-19.

[18] Ibid., 19-20.

[19] China and the Soviet Union, and later the Russian Federation.

[20] Vine, David, ‘Where in the world is the U.S. military?’, Politico (August 2015) https://web.archive.org/web/20190208095355/http://www.politico.com/magazine/story/2015/06/us-military-bases-around-the-world-119321.

[21] Since the US can create dollars, it will never not be able to pay off a dollar loan, as it can simply create the money needed for repayment.

However, other debtor countries, like Pakistan, for instance, cannot print dollars. Instead, if they fall into trouble, they are made to cut back state spending and raise taxes on their population. This revenue accrues in local currency, which is then thrown onto foreign exchange markets to buy dollars to then pay the debt. This stimulates demand for the dollar but increases the supply of the local currency on forex markets, which can lead it to become devalued.

[22] Wong, Andrea, ‘The untold story behind Saudi Arabia’s 41-year debt secret’, Bloomberg (30 May 2016) https://archive.md/b2vPx.

[23] In the Cold War sense of the term. ‘Third World’ in this context means countries that did not fall easily into the First World (Western sphere) or Second World (Soviet sphere). The Third World had substantial influence over the UN General Assembly but could not counteract the influence of the Security Council, where the great powers held court.

[24] Declaration on the Establishment of a New International Economic Order, GA, UN Doc A/RES/3201(S-VI) (adopted 1 May 1974) https://digitallibrary.un.org/record/218450?ln=en#record-files-collapse-header.

[25] This is the thesis of Adam Smith’s The Wealth of Nations (1776). Smith was critical of mercantilist policies that prioritised the collection of precious metals in the treasury above developing actual productive capacity. While precious metals no longer play a central role in global trade, the principle about developing productive capacity holds true. Smith is quoted a lot, but not many people actually read him.

[26] Hudson, 29.

[27] Hirsch, Paddy and Darian Woods, ‘China’s slice of the US debt pie’, NPR (23 August 2022) https://www.npr.org/2022/08/23/1119126863/chinas-slice-of-the-us-debt-pie.

[28] Taylor, Timothy, ‘The US Treasury review of economic sanctions’, Conversable Economist (blog, 9 December 2021) https://conversableeconomist.com/2021/12/09/the-us-treasury-review-of-economic-sanctions/.

[29] Hudson, 444.

[30] Iran in 1979, Venezuela in 2019, Afghanistan in 2021. These assets are still frozen.

[31] Shakil, F.M., ‘By the numbers: The de-dollarization of global trade’, The Cradle (13 January 2023) https://thecradle.co/article-view/20279.

[32] Cusack, John, ‘Where are the sanctioned Russian assets frozen in the West and how much is actually frozen?’, Financial Crime News (23 February 2023) https://thefinancialcrimenews.com/where-are-the-sanctioned-russian-assets-frozen-in-the-west-and-how-much-is-actually-frozen/.

[33] Most people who support Ukraine do not intuitively have a problem with this. The problem, though, is that writing retroactive laws is generally regarded as being against the rule of law. And the main point of the rule of law, economically speaking, is to provide certainty. That is why financial institutions like banks are so heavily regulated.

People are finicky about money and will withdraw their deposits if they think their assets are liable to be seized arbitrarily or without warning. It’s more about simple risk calculation than about whether the entity that had its assets seized ‘deserved’ it or not. When it comes to finance and banking, ‘deserve’ has nothing to do with it.

[34] Yellen, Janet (Treasury Secretary, United States) interviewed by Fareed Zakaria, CNN (YouTube video, 17 April 2023) https://youtu.be/bwgHwzhfoXo?t=218.

[35] Ordinarily, currency figures are converted into USD. Though here, they remain in CNY, since the fact that this money is in renminbi, not dollars, is the substantive point.

[36] Banco Central de la República Argentina, ‘El BCRA y el PBC confirman activación especial del swap de monedas’ (release, 8 January 2023) https://web.archive.org/web/20230206225617/https://bcra.gob.ar/noticias/El-BCRA-y-el-PBC-confirman-activacion-especial-del-swap-de-monedas.asp.

[37] Paraskova, Tsvetana, ‘China settles first LNG trade in yuan’, OIlPrice.com (29 March 2023) https://oilprice.com/Latest-Energy-News/World-News/China-Settles-First-LNG-Trade-In-Yuan.html.

[38] Shakil.

[39] Business Standard, ‘BRICS mulling alternative to dollar-dominated payment system: South Africa’ (19 January 2023) https://www.business-standard.com/article/economy-policy/brics-mulling-alternative-to-dollar-dominated-payment-system-south-africa-123011900244_1.html.

Lula da Silva recently expressed similar sentiments.

[40] Silk Road Briefing, ‘Brazil & China sign agreement to drop US dollar and use RMB yuan – real in bilateral trade’ (31 March 2023) https://www.silkroadbriefing.com/news/2023/03/31/brazil-china-sign-agreement-to-drop-us-dollar-and-use-rmb-yuan-real-in-bilateral-trade.

[41] Rousseff, Dilma (President of New Development Bank) interviewed by Wu Lei, CGTN (YouTube video, 15 April 2023) https://youtu.be/qe2GiD5fCQY.

[42] Times of India, ’19 countries express interest in joining BRICS group’ (25 April 2023) https://timesofindia.indiatimes.com/world/rest-of-world/19-countries-express-interest-in-joining-brics-group/articleshow/99756285.cms?from=mdr.

[43] Bertaut, Carol, Bastian von Beschwitz, and Stephanie Curcuru, ‘The international role of the US dollar’, FEDS Notes (research report, United States Federal Reserve, 6 October 2021) https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-20211006.html.

On a side note, the reason the euro will never become a global reserve currency is that Eurozone rules place strict limits on deficit spending. This means that Eurozone countries cannot run the kind of persistent payments deficits that flooded the world with US dollars and converted it into the global reserve currency.

[44] Pozsar, Zoltan, ‘Great power conflict puts the dollar’s exorbitant privilege under threat’, Financial Times (20 January 2023) https://archive.is/20230128065634/https://www.ft.com/content/3e05b491-d781-4865-b0f7-777bc95ebf71.

[45] Gold is an effectively sanctions-proof as a means of settlement, as unlike money, it is not a form of government debt and cannot be canceled or unilaterally destroyed. And it cannot be seized other than physically. It is largely useless for domestic transactions but quite useful for cross-border, bulk transactions. This is why Germany has recently repatriated much of its gold holdings to its own territory. And this is also why it was a bad idea for Venezuela to hold its gold reserves at the Bank of England.

To the disappointment of gold-bugs, though, it can only be an expedient. Attempts to reintroduce a gold standard will bring back the problems related to persistent BoP imbalances outlined earlier. Also, economic expansion needs to be accompanied by money supply expansion, which causes problems if gold forms the monetary base since it is finite.

[46] Bloomberg, ‘China expands gold reserves at central bank for fifth month’ (7 April 2023) https://archive.is/20230407090807/https://www.bloomberg.com/news/articles/2023-04-07/china-expands-gold-reserves-at-central-bank-for-fifth-month#xj4y7vzkg.

The number given for China’s gold reserves is 2068 tons, equivalent to around 1876 metric tonnes.

[47] Duguid, Kate and Nikou Asgari, ‘Central banks look to China’s renminbi to diversify foreign currency reserves’, Financial Times (1 July 2022) https://archive.is/20220701011247/https://www.ft.com/content/ce09687f-f7e5-499a-9521-d98cbd4c5ac1#selection-1487.0-1487.77.

[48] ‘Exorbitant privilege’ is the term used by French officials to describe the dollar’s role in US primacy. Though, I’m sure Africans feel the same way about the CFA franc.

[49] Senator Marco Rubio was quite candid about this in a recent interview. See Marco Rubio (United States Senator – Florida) interviewed by Sean Hannity, Fox News (30 March 2023) https://www.youtube.com/watch?v=6culYsSCAyI&t=136s.

Related Posts

The red herring of the ‘war on Hamas’

Washington pushes China out of the internet

It’s an interesting article. Where can I learn more about dollar hegemony? Would you recommend reputable sources?

Hi Elly. Sorry about my late reply, I’ve been offline for a while. The best book to learn about this topic is probably ‘Super-Imperialism: The Economic Strategy of American Empire’ by Michael Hudson. You should be able to find the details in the source list.